|

Guest Article

The Impact Financial Education Has On Plan Participant Saving and Investing BehaviorBy Liz Davidson, founder and CEO of Financial Finesse. Increasingly, participant retirement education is being evaluated with the bottom line in mind, with companies demanding that the programs they roll out to their employees actually change behavior. It is about time for us to begin to track the statistical success of these programs, to evaluate them on the bottom line numbers and to ask the tough questions, namely:

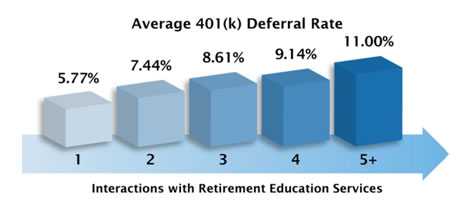

Years ago, when more employers had defined benefit plans, stock options, more generous profit sharing and plan matching programs, you could argue that there was little or no need for employees to change their financial behavior in order to reach their retirement goals. Instead, plan sponsors focused on marketing their retirement benefits so employees fully appreciated the value of the benefits, and by extension, their jobs overall. My, how times have changed. Today, only 31% of employees are offered a traditional pension plan and, for those that work in the private sector, pension payouts typically fund only a portion of their retirement income needs. In a society where the average savings rate is just above 5%, 50% of people don't know the basics about stocks, bonds and mutual funds, and life expectancy for those that reach retirement is 85, employees are at a huge disadvantage when it comes to building adequate retirement savings. If you consider how unprepared employees are for this newfound responsibility, with 83% admitting they are not on track to meet their retirement goals, it becomes obvious why the standards for retirement communication and education are changing. It's no longer enough that your employees really like a workshop, say they appreciate the guidance they received from a one-on-one financial planning session, or comment on how "cool" the online retirement planning calculator is. They must actually take action on what they learn or they will not be able to retire. After all, if they can't retire, your company pays the price-estimated at an additional $10,000-$50,000 per employee for every year an employee postpones retirement (mostly health care and higher salaries that more tenured employees earn vs. less tenured employees that would otherwise replace them). Bottom line-any retirement planning education you roll out to your employees must have a significant and enduring impact on participant behavior in order to be successful. Our research shows that 92% of employees who participate in retirement education make a major change to their retirement plans within 30 days of receiving the education. The most common changes are to increase retirement savings, reallocate their assets to be more appropriate to their time horizon and goals, and open up a Roth or Traditional IRA to supplement their company-sponsored plans. More significantly, there is a direct correlation between financial education and deferral rates. The more times an employee receives retirement education, the higher the deferral rate.

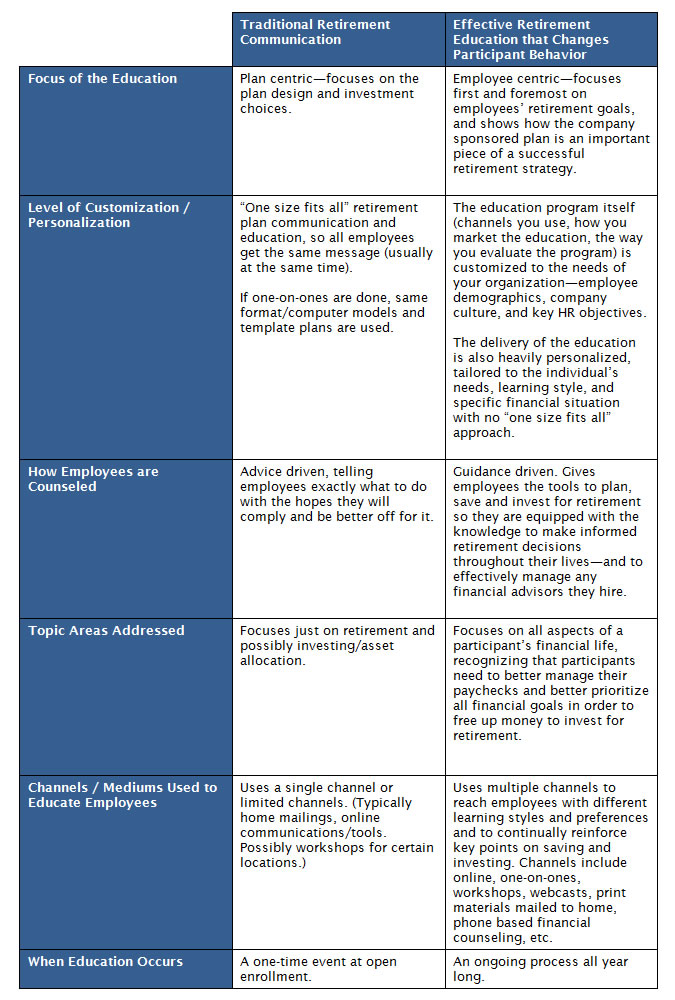

So, what do companies need to do to get these results and ultimately, avoid a major retirement crisis? The first and most important step is for the investment committee to shift their perspective from solving the problem with traditional retirement plan communication to implementing an ongoing retirement education program that is designed to change behavior. Below is a table outlining the difference between traditional retirement communication, which informs employees about their retirement plans, and retirement education programs that effect long term behavioral change-the kind of change that is needed in order for employees to effectively prepare for retirement. While this doesn't outline all best practices associated with developing a successful retirement education, it does provide a framework for HR and retirement benefits managers to use as they evaluate different retirement education programs:

About Financial Finesse

Financial Finesse was founded with a single mission: Provide people with the information they need to become financially independent and secure. Today, we are the leading provider of unbiased financial education for large companies and municipalities. Our financial education services are fully integrated programs designed to address the strategic goals of the organizations we service and are delivered by on-staff CERTIFIED FINANCIAL PLANNER™ professionals as an employee benefit. If you are interested in learning more about workplace financial education programs, contact one of our education consultants at AskFF@financialfinesse.com. The Ask Financial Finesse Q&A service is designed to provide general information on trends and developments in workplace financial education programs and participant education strategies. Due to the complex nature of financial benefits and/or workplace financial issues, the information contained in this document is not to be construed as advice. ### 401khelpcenter.com is not affiliated with the author of this article nor responsible for its content. The opinions expressed here are those of the author and do not necessarily reflect the positions of 401khelpcenter.com. | ||||

|

About

| Glossary

| Privacy Policy

| Terms of Use

| Contact Us

|